NBFCs to face higher fund costs as banks look to pass on MCLR hikes

December 21, 2022

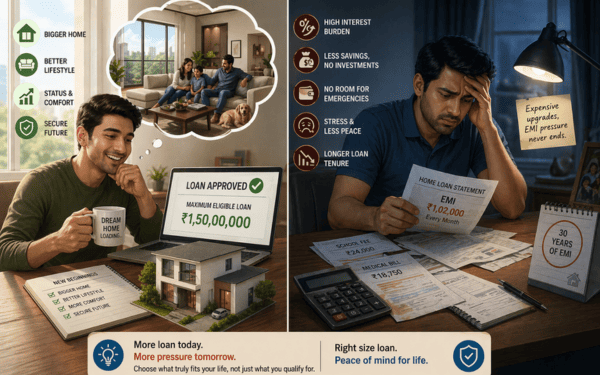

In most cases, home buyers consider the sanctioned loan amount as an indicative figure when applying for a home loan. As they find the loan sanction amount higher, they think it is safe to take such a home loan considering their capacity to repay it without difficulties. However, the eligibility criteria considered for a loan does not fully take into account the real financial state of an individual. Thus, taking an amount higher than required would make a person experience serious difficulties.

Increased EMI leads to lower flexibility

It is evident that a larger loan results in an increased EMI, where the majority of the monthly salary gets tied up in monthly EMI payments. This implies that there would not be enough money left for personal investment, saving, and other expenditure.

Even when the EMI seems affordable, the reduced financial flexibility would become a challenge in the future after having several more financial commitments.

Costly to repay due to increased loan tenure

It is clear that taking a higher amount loan would not only mean that the loan principal is high, but it would also imply that the interest amount charged on the entire period of the loan would be higher.

As the tenure of home loans is usually very high, a small increase in the loan amount can lead to a huge interest amount charged over many years.

Delayed achievement of future financial plans

Having to pay a higher EMI, which would consume a major part of the monthly salary, might delay achieving other future financial goals. The financial goals may include retirement investments, children's education, traveling, business ventures, and emergency funds among others.

Thus, failure to meet such goals could result from taking a big amount of home loan.

Increased income would not necessarily help

Most individuals assume that increased income levels would enable them to meet the EMI requirements comfortably. Even though income usually tends to rise as time goes by, this is not always true.

Several factors may prevent an individual from increasing his income, including changes in career or work environment, lifestyle changes, and health issues among others.

Expenses may also rise in the future

As individuals get married and start having children, expenses tend to escalate quite rapidly. In addition, other factors like increased costs associated with medical care and ageing parents may contribute to such expenses.

Thus, a home loan amount that was previously affordable would turn out to be costly after a number of years.

Take a smaller loan amount

It is recommended that an individual borrows what he is comfortable with and not what the lending institution qualifies him for. This ensures that the individual can live comfortably while meeting all other financial obligations in the future.

Therefore, it is advisable to have a house which does not dominate your life.

Source : By MONEYCONTROL PF TEAM

{kind=link}